ELEVATE responsible sourcing risk outlook 2021 shows heightened supply chain risks in key sourcing markets

The 2021 risk scores come as the interest from global buyers and investors in sustainability, ESG, and supply chain risks continue to soar. 2020 has been an unprecedented year for the supply chain:

- Covid-19 continues to affect business continuity, supplier margins, and worker livelihoods around the world

- Media and NGO exposés highlight the risk of modern slavery in supply chains

- The U.S. Customs and Border Protection (CBP) increasing use of Withhold Release Orders (WROs) for forced labor (WROs)

These three factors, and related issues, have increased operational and compliance risks in the supply chain leading global stakeholders and businesses to step up their efforts in due diligence and product traceability.

ELEVATE 2021 Risk Scores are built on social and environmental assessment data coming from workplaces (factories, farms, logistics centers), non-traditional big data (web data harvesting), and public domain datasets. Blending these different, complementing data sources, ELEVATE built a comprehensive and predictive assessment of global supply risk across five dimensions: Labor, Environment, Business Ethics, Management Systems, and Health and Safety (H&S). This data is used to provide stakeholders with an unbiased, transparent risk assessment of their operations and investments.

COVID-19 has made the S in ESG a critical risk factor for global buyers and investors

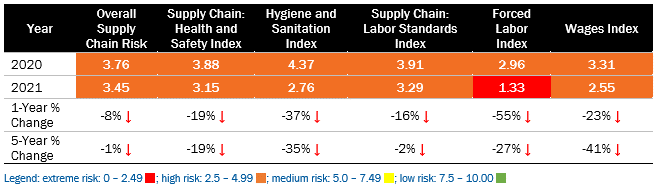

Table 1. Overall Supply Chain Risk Score and key indices; 1-Year % Changes; 5-Year % Changes – Countries with 50%+ confidence level

The ELEVATE 2021 overall Supply Chain Risk Score deteriorated by -8% compared to the 2020 score.

H&S is the area with the largest overall score deterioration as workplaces around the world struggle to contain COVID-19 and to adapt to new H&S regulations. ELEVATE’s Health & Safety Index dropped globally by 19% vs. 2020. This was driven by a significant deterioration in the Hygiene and Sanitation Index (-37%) as the indicator most connected to sanitary conditions and virus containment in workplaces including in canteen and dormitories.

Likewise, COVID-19 led to operational and financial disruption around the globe – such as retailer order cancellations and the consequential impact on manufacturer business continuity and worker livelihood. The Labor Standards Index – which includes ELEVATE key indicators such as wages, freedom of association, and forced labor – decreased by -16% compared to the previous year.

Sourcing risk increased in legacy markets, while no significant improvements in emerging supply chain

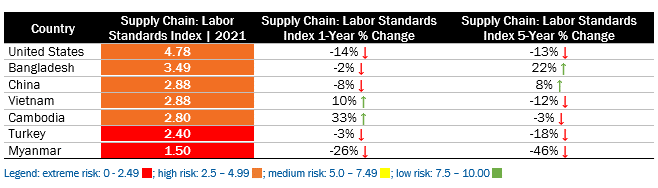

Table 2. Labor Standard Index– 2021 Risk; 1-Year % Changes; 5-Year % Changes

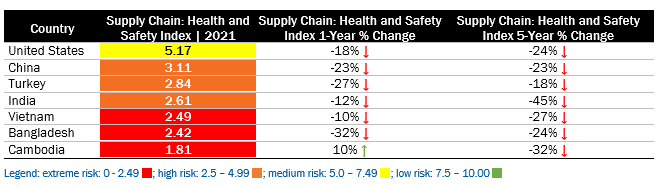

Table 3. Health and Safety Index– 2021 Risk; 1-Year % Changes; 5-Year % Changes

COVID-19 has exposed numerous vulnerabilities across working standards in countries with long-standing, established exporting sectors. Among these, China, India, Bangladesh, and United States have experienced a drop in the labor and health and safety indices in part driven by the pandemic – i.e. increased non-compliances in wage payments and deteriorated hygiene conditions in the dormitory or workplace.

Countries that have experienced recent success in export-oriented and low-value sectors (i.e. apparel) present on average extreme risk in labor standards. This is the case for Turkey and Myanmar that present extreme risk and 5-year negative trends in key areas such as abuses and discrimination, freedom of association, wage payment compliance, and forced labor.

Still, emerging markets such as Vietnam and Cambodia present extreme H&S risk and a 5-year downward trend related to safety conditions in the workplace. Risk has aggravated especially in key areas such as hygiene and sanitation, chemical management practices, and occupational safety.

Global buyers visibility over real conditions in key supply chains remains critical

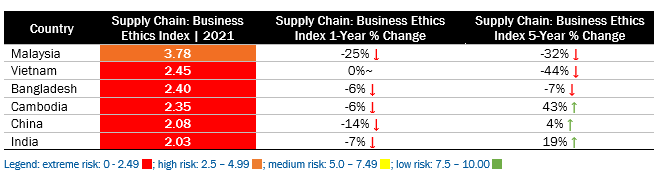

Table 4. Business Ethics Index– 2021 Risk; 1-Year % Changes; 5-Year % Changes

Factory managers integrity during on-site audit activities – i.e. coaching workers for interviews, attempt briberies – is a fundamental first step to identifying and improving working conditions in the supply chain. In key Asian countries, economic disruption due to the pandemic saw a deterioration of the integrity practices relative to other sourcing markets. Malaysia experienced the largest drop in the Business Ethics risk index (-25%), followed by China (-14%), Bangladesh (-6%), and India (-7%). In China specifically, in 2020 the percentage of audits deemed transparent by our auditors dropped by 12% compared to 2019.

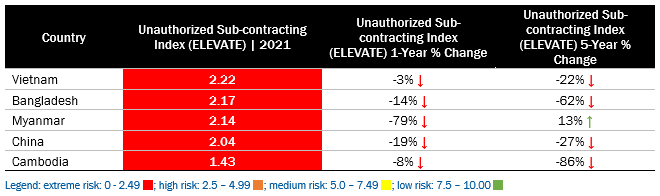

Trade tensions and Covid-19 are increasing risk related to supply chain traceability

Table 5. Unauthorized Subcontracting Index– 2021 Risk: 1-Year % Changes; 5-Year % Changes

In the past 5 years, the increasing trade risk and increasing labor costs have pushed global buyers to diversify their supply chains away from China. This is the case for buyers in apparel and electronics that are placing more orders in Vietnam, Cambodia, Bangladesh, and homeshoring ¹. But this increased demand has knock-on implications including an increase in unauthorized subcontracting risk – the risk of the contracted manufacturer subcontracting orders to unauthorized third suppliers in order to support production or increase margins. The risk of unauthorized subcontracting is further aggravated by COVID-19. To comply with the new H&S regulations in response to the pandemic, suppliers must comply with new H&S restrictions that reduce production capacity e.g. social distancing and alternating work shifts. Textile and apparel suppliers are particularly at risk as many have recently shifted their production to Protective Personal Equipment (PPE) ². As demand for PPE has grown by an average of more than 50% since April 2020, factories that have converted part of their production to mask and gowns are at risk of subcontracting fashion orders to keep up with the demand.

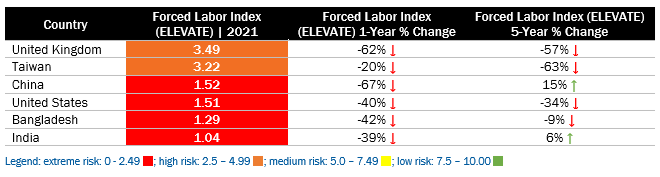

Forced labor is on the rise across the supply chain especially for lower tiers

Table 6. Forced Labor Index– 2021 Risk: 1-Year % Changes; 5-Year % Changes

Despite the international regulations passed in the last decade, ELEVATE data reports an increased risk of forced labor among vulnerable populations in key sourcing countries. This includes ethnic minorities in China, foreign migrant workers in the United States and Malaysia, as well as adolescent women in India. Key Asian supply chain countries have experienced a deterioration in the Forced Labor Index scores: China is down (-67%), and India (-39%). Forced labor practices are also on the rise in advanced supply chains such as the United States (-40%) and the United Kingdom (-62%) due to the repeated exploitations of vulnerable populations in the apparel, food, and agricultural supply chain. Many of these workers are foreign or domestic migrants that have entered the supply chain via a labor broker, may have paid fees for a job, and are living in poor quality dormitories provided by the supplier.

The risk ahead: emerging political risk in the Greater Mekong area

Table 7. Freedom of Association and Human Treatment Indices – Risk Categories and 1-Year Percentage Changes

Myanmar and Cambodia are both countries facing significant political risk and pressure from the international community for the respect of workers and human rights.

Myanmar is among the bottom 10 percentile of countries under labor standards. Forced labor, freedom of association, and humane treatment (risk of verbal and/or sexual harassment and abuse in the workplace) are all extreme risks. In the light of the recent military coup, we expect a significant increase in labor risks especially relating to freedom of association and humane treatment.

The Cambodian government used the Covid-19 pandemic as a pretext to further tighten its political control. During 2020, the government repeatedly resorted to violence and arrests against the opposition, human rights defenders, and the press. The results of this authoritarian push were reflected in increased risks relating to freedom of association (-33%) and humane treatment (-17%). These factors may be exacerbated in 2021 as continued instability in Myanmar could motivate increased migration of workers into neighboring countries such as Cambodia, Thailand, and Viet Nam.

[1] UNCTAD, Global Trade Update: February 2021- https://unctad.org/system/files/official-document/ditcinf2021d1_en.pdf

[2] UNCTAD, Global Trade Update: October 2020- https://unctad.org/webflyer/global-trade-update-october-2020

These blogs are written by ELEVATE staff members or associates and the views and opinions expressed are not necessarily those of ELEVATE.

About the authors