New countries, new risks: How to anticipate, manage and minimize risks in new sourcing markets

The ongoing trade war and increased labor costs are increasingly motivating companies to evaluate additional sourcing destinations outside China and sometimes new product areas. This trend is likely to continue even if some form of trade agreement is finalized. While these alternative sourcing locations could generate significant returns, they also present new and unexpected risks to corporate supply chains.

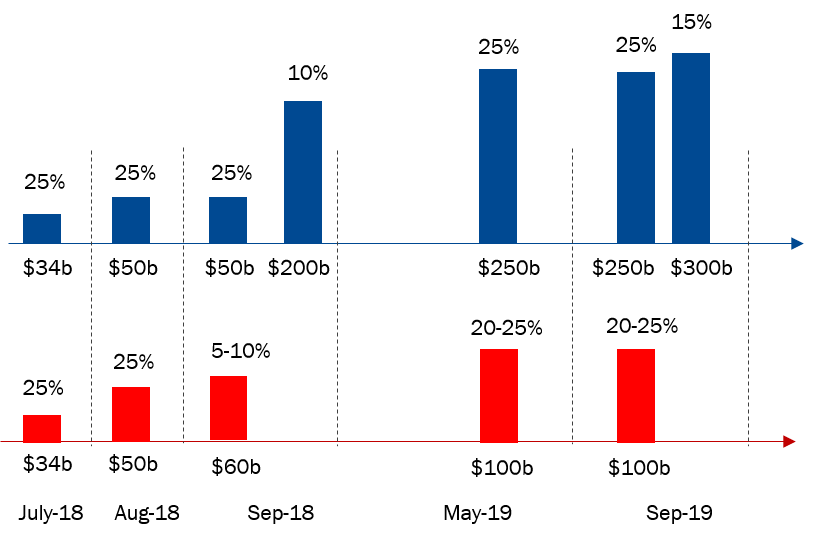

Since 2018, the Trump administration has engaged in a trade war with China. In July 2018, Trump imposed 25% tariffs on Chinese goods worth USD34 billion dollars. China responded with taxes on US goods and as of September 2019, tariffs have been placed on USD550 billion worth of Chinese goods and USD100 billion worth of US goods.

Figure 1 below illustrates the value of targeted goods (USD) and the % of values that tariffs represent for the US and China.

US (blue) and China (red) tariffs

Values of targeted goods and % of tariff imposed

Source: internal calculations

The US has imposed tariffs on a wide range of products including electrical equipment, clothing, footwear, dishwashers, flat panel TVs, etc. On the other hand, China put tariffs on key imports from the US market such as electric / hybrid vehicles and agricultural goods such as soybeans.

Besides the trade war, increasing labor costs as a result of workforce shortages is also increasing the competitive advantage and appeal of those neighboring countries that have just recently started the industrialization process e.g. Cambodia, Myanmar, and Vietnam. Low wages, a young workforce and reduced tariffs make these new markets more interesting to brands than previously.

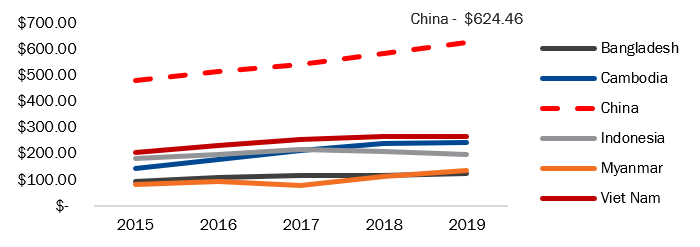

Figure 2 below illustrates that Chinese take-home salaries in the apparel, accessories and footwear industry are more than twice as high as those in Vietnam. Vietnam is the second most expensive in terms of labor cost in the traditional sourcing markets considered below.

Monthly Wages in the Apparel, Footwear and Accessories (USD)

Source: ELEVATE (2019). EiQ: Dimensional Risk, 2019. http://www.elevatelimited.com/services/analytics/eiq/

Moving to low cost countries presents significant economic opportunities for brands that seek lower production costs and want to avoid new tariffs. But shifting the supply chain to new geographies may come with different or more significant social and environmental compliance risks. This is pertinent because of the increasing scrutiny placed on brands and retailers by investors, civil society organizations and NGOs to address this challenge. Collaboration with peers and participation in industry initiatives are increasingly supporting brands to mitigate the prevailing risks in their supply chains.

But how do we address risks in regions that are unfamiliar to us? What do we do with emerging risks in supply chains?

This requires a deeper understanding of prevailing issues on the ground in these regions. At ELEVATE, we have been collecting and compiling assessment data for more than 10 years and evaluating compliance trends. We blend these data sets with publicly available risk data to estimate the exposure of risk at country and industry level, and have run a series of simulations on how we expect risk to change for low and high-value chain brands that move out of China to neighboring markets.

Low-value chain industries will experience more risk as they move away from China

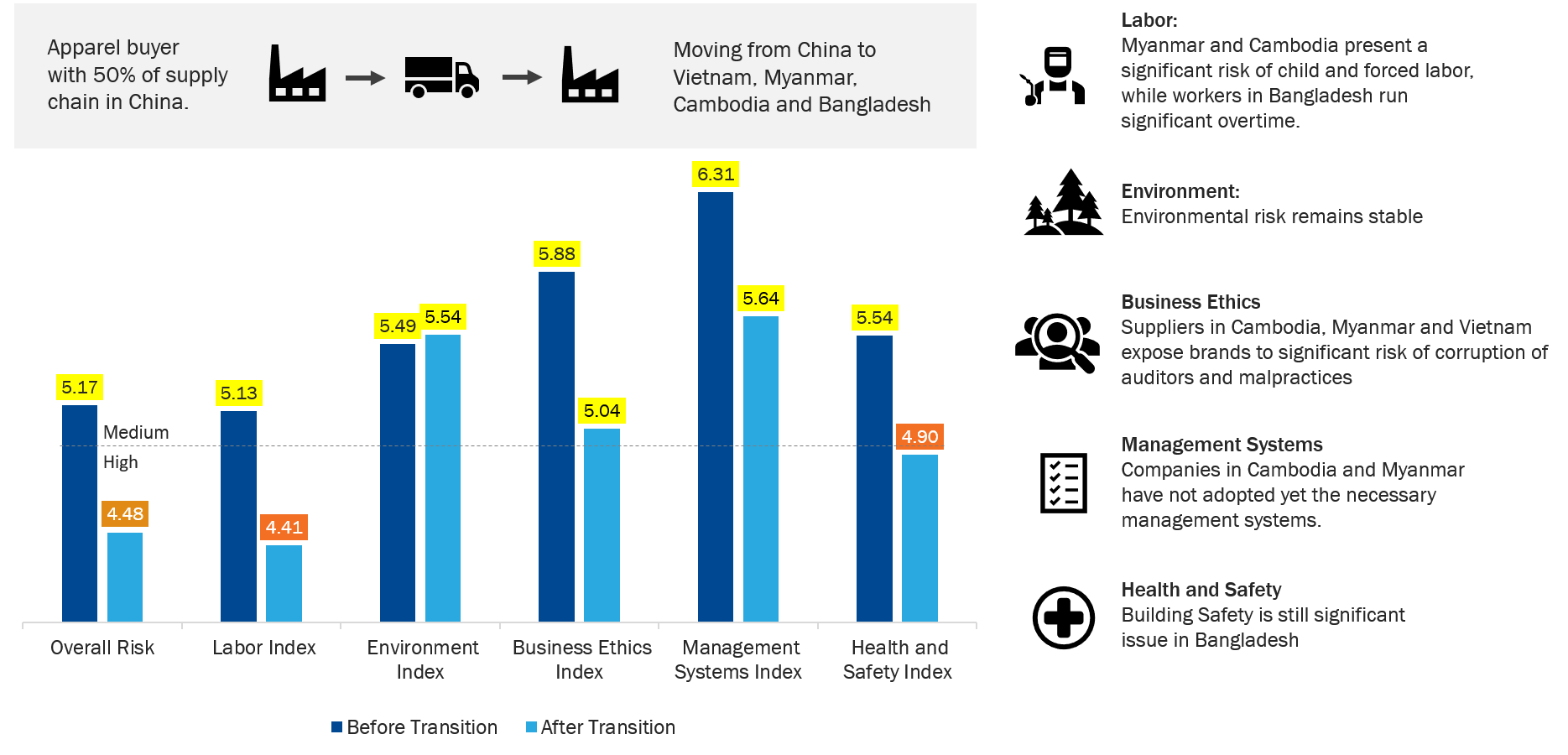

Case 1: Apparel companies moving from China to countries such as Myanmar, Cambodia, Vietnam and Bangladesh are going to experience significantly lower production costs but at the same time face increasing compliance risk. When compared to China, geographies like Myanmar and Cambodia present a higher risk of zero tolerance violations such as child and forced labor. Workers in Bangladesh have significantly higher overtime hours compared to China. Myanmar and Vietnam also expose brands to significant risk of corruption (bribery of auditors) and other poor documentation practices.

Figure 3 below plots the supplier portfolio risk on a bar graph where the dark blue indicates the exposure to risk before the transition and the light blue after the transition from China. We see that risk increases from medium to high, especially because of labor risk and health and safety risk.

Source: ELEVATE (2019). EiQ: Dimensional Risk, 2019. http://www.elevatelimited.com/services/analytics/eiq/

Risk for high-value chain industries might not change in intensity but will change in type

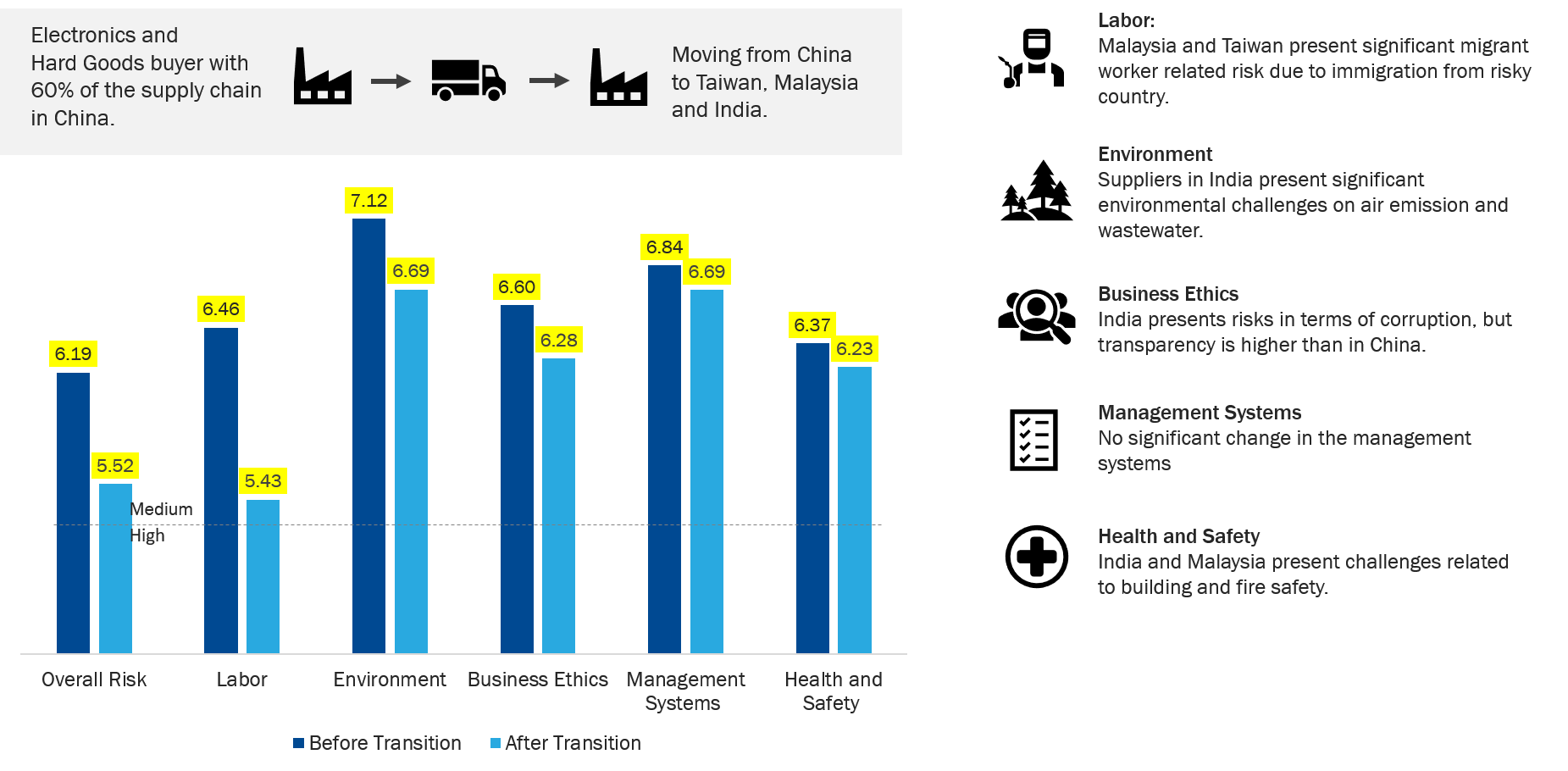

Case 2: Electronics and other higher value chain companies moving from China to competing markets such as Taiwan, Malaysia and India are going to experience a similar level, but different type, of compliance risk. For example, countries such as Malaysia and Taiwan present more migrant worker-related risks due to the migration of workers from countries that have poor regulatory standards e.g. Vietnam, Bangladesh, Nepal, Cambodia, etc. The Indian supply chain also presents a larger risk in terms of corruption of auditors and worker health and safety (H&S).

Figure 4 below shows how we have platted the supplier portfolio risk on a bar graph with the dark blue indicating the exposure to risk before the transition and the light blue after the transition from China. We see that risk increases from medium to high, especially in labor and ethics.

Source: ELEVATE (2019). EiQ: Dimensional Risk, 2019. http://www.elevatelimited.com/services/analytics/eiq/

Risk profiles change as more companies enter emerging markets

Figure 5 below shows a strong correlation between production costs (evidenced by take home salary) and compliance risk. Geographies with higher production costs are typically associated with lower compliance risks. On the other hand, lower salaries correlate with higher compliance risks.

In this graph, we have plotted risk against production costs (proxied by salary level) in the electronics, toy and hard good sectors across key supply chain countries. Countries above the fitting line present a positive trade-off for brands: lower sourcing risk given the production cost they charge. Countries south of the fitting line present production costs that are excessively high given the risk posed by factories.

Production Cost and Risk: Electronics, Toys, Hard Goods – across countries – 2019

Monthly take home salary (USD)

Source: ELEVATE (2019). EiQ: Monthly take home salary, Overall Risk, 2019. http://www.elevatelimited.com/services/analytics/eiq/

China is a significant outlier in this relationship presenting both high costs and high sourcing risk. Why? China offers significant production advantages when compared to competing countries in the Asian supply chain. These include access to raw materials and components, know-how, productivity levels and product quality. Companies that move away from China to emerging markets will likely contribute to an increased production pressure on local suppliers and may potentially increase the risk of unauthorized subcontracting to meet this production demand. Excessive overtime and negligent H&S standards in the workplace are also likely to increase. As more brands shift their supply chain, we foresee increasing risk in the emerging markets.

Moving forward: setting priorities, leveraging data, re-assessing risk

Data can support brands in their journey to manage risk and implement an effective program i.e. run a compliant and resilient supply chain that optimizes resources. Here are a few steps on how to effectively identify and address risks in your supply chain.

- The first step is to assess risk appetite – evaluate risks in existing countries in your supply chain and determine how much risk your company is willing to accept. This includes assessing the regulatory risk in sourcing markets (e.g. recruiting norms in Malaysia) and reporting norms (e.g. the Modern Slavery Act for Australian and UK brands).

- The second step is to assess risk based on audit and publicly available data (e.g. World Bank, United Nations, etc.). Based on risk information and internal business metrics such as volume of orders and dollar spend, brands can rank / assess suppliers based on business relationship / importance (e.g. strategic or transactional).

- Lastly, based on exposure to risk and the importance of business relationships with suppliers, responsible sourcing departments can implement different strategies or levels of engagement for specific supplier groups. These include, for example, audit prioritization, investment in corrective action plans, and training programs.

The responsible sourcing journey does not end here. With the rapid changes in the global supply chain, we expect a dynamic risk landscape. Keeping abreast with emerging risks will require brands and retailers to continuously monitor and re-assess risk in their supply chain.

ELEVATE’s EiQ delivers the supply chain intelligence needed to be across the risk landscape and sustain transformation in your programs.

Learn more about EiQ benefits

These blogs are written by ELEVATE staff members or associates and the views and opinions expressed are not necessarily those of ELEVATE.

About the authors