Climate change impact on the real estate industry in Asia

Recent extreme weather events have caused significant physical damage to properties and infrastructure. Damages and losses from natural disasters caused insurers to pay out a record USD 135 billion globally in 2017[1]. According to National Oceanic and Atmospheric Administration estimations[2], this figure does not represent actual damages, which it values at USD 307 billion in the United States alone.

Assets’ exposure to climate risks

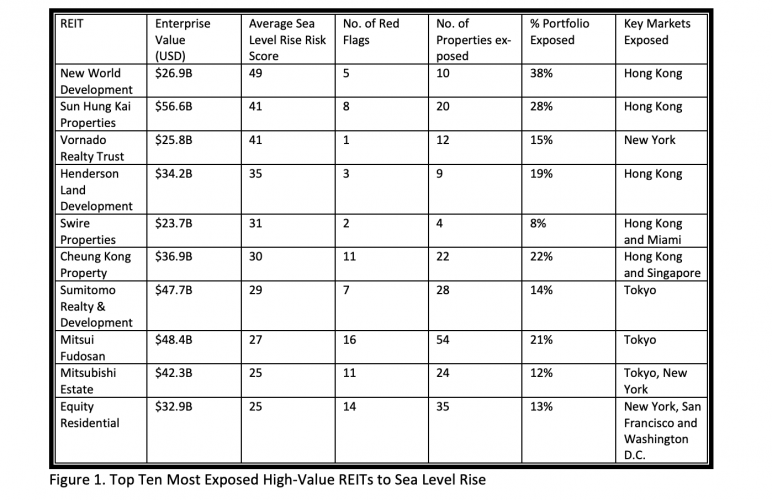

According to a recent research paper “Climate Risk, Real Estate, and the Bottom Line”, eight out of ten of the most exposed high-value Real Estate Investment Trusts (REITs) to sea level rise are in Asia. Five out of ten have properties in Hong Kong (see Figure 1). One of the key takeaways from the paper is that overall, 35% of REITs properties are exposed to climate hazards, of these, 17% are exposed to inland flood risk, 6% to sea level rise and coastal floods, and 12% exposed to hurricanes or typhoons.

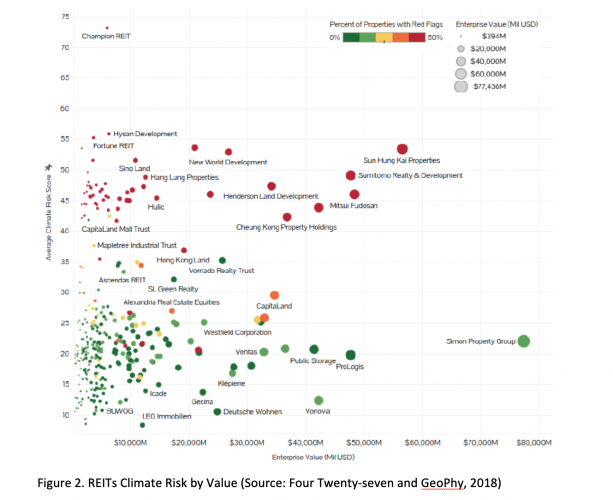

In addition, REITs concentrated in Hong Kong and Singapore display the highest exposure to rising seas. Sun Hung Kai Properties, worth USD 56 billion, has over a quarter of its properties exposed to coastal flooding and its regional peers also face high levels of climate hazards including (sea level rise, hurricanes and typhoons, flood, water stress, heat stress) (see Figure 2).

Failure to address and mitigate climate related risks may result in increased exposure to loss due to assets suffering from reduced liquidity as well as lower income, which will negatively affect investment returns[3].

Property devaluation and the limitations of insurance

Studies focused on residential markets in Florida, Germany and Finland found that properties exposed to sea-level rise or flood risk have seen values grow at a reduced rate compare to similar properties without flood risk[4]. Similar impacts were observed in the United States, with properties exposed to sea-level rise selling at a 7 % discount to those with less exposure.

Insurance is routinely considered as one of the best protective measures for climate related risks. While it has provided for coverage for most damages from catastrophic events, it cannot protect them from a reduction in an asset’s liquidity or deprecation in value. Hence, using insurance as the main protection for asset value is not an effective solution to reduce the risk of devaluation, especially due to premiums which are largely based on historical analysis and are not likely to consider future climate risks.

The way forward

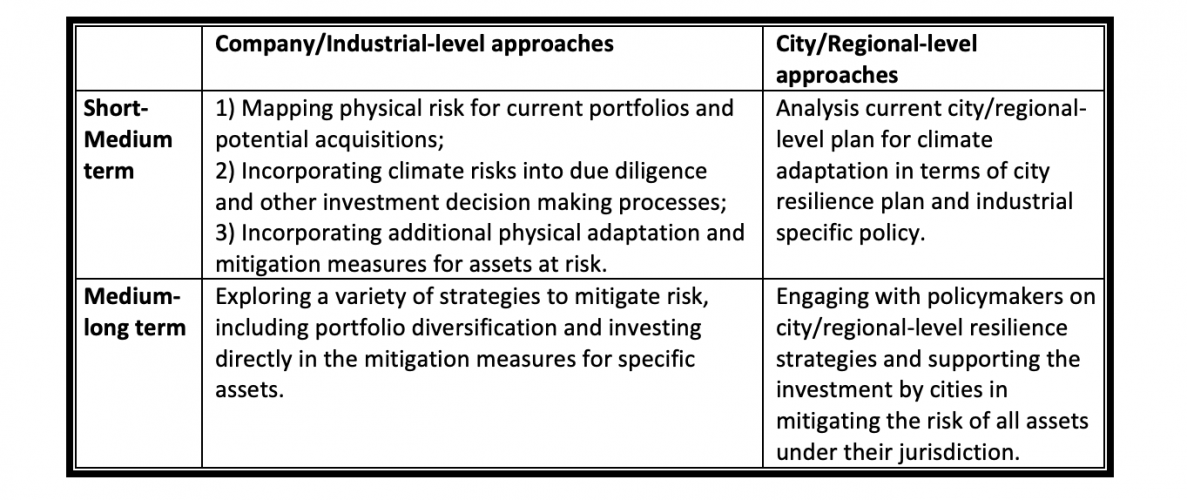

The real estate investment industry as a whole is still early in its development of strategies to identify, understand, and manage climate-related risks. The industry needs to be able to better measure the value impact so it can base its future decision-making on a quantitative rather than qualitative understanding of the risks and the potential return from investing in mitigation strategies for their assets.

On the other hand, a recent research paper, “climate risk and real estate investment decision making”, indicated that risks such as sea-level rise and heat stress will increasingly highlight the vulnerability not only of individual assets and locations, but of entire metropolitan areas. Building for resilience, on a portfolio, property and citywide basis would become imperative to staying competitive in the near future[5]. Therefore, understanding city- and regional-level climate resilience and engaging with local policymakers is a key part of understanding the risks and impacts of one’s portfolios.

More and more investors and investment managers are exploring new ways to find better tools and common standards to help the industry get better at understanding climate related financial impacts in the future. Some approaches under exploration worldwide are[6]:

Reporting on climate impacts and mitigation measures

Companies have been reporting on their overall sustainability and climate mitigation efforts through various global reporting frameworks such as the Global Reporting Initiative, Carbon Disclosure Project (CDP) and the real estate industry specific Global Real Estate Sustainability Benchmark (BRESB) amongst others. However, proactive companies from the real estate industry such as City Developments Limited and CapitaLand[7] are already responding to the growing demand from investors and other stakeholders and are reporting on their climate related financial risks and opportunities using the Task Force on Climate-Related Disclosure (TCFD).

Companies showing support for TCFD and beginning to disclose decision-useful information to investors resulted in positive market momentum. From an investor or lender’s point of view, reporting on TCFD increase their confidence that the firm’s climate related risks are appropriately assessed and managed; from a company’ prospective, the increased awareness and understanding of climate related risks and opportunities within company resulting in better risk management and more informed strategic planning.

To learn how CSR Asia can help you to report on TCFD’s recommended disclosures, contact li.fan@elevatelimited.com.

[1] Hiroko Tabuchi, “2017 Set a Record for Losses from Natural Disasters. It Could Get Worse,” New York Times, January 4, 2018, https://www.nytimes.com/2018/01/04/climate/losses-natural-disasters-insurance.html.

[2] Adam B. Smith, “2017 U.S. Billion-Dollar Weather and Climate Disasters: A Historic Year in Context,” Climate.gov, January 8, 2018, https://www.climate.gov/news-features/blogs/beyond-data/2017-us-billion-dollar-weather-and-climate-disasters-historic-year.

[3] http://www.heitman.com/wp-content/uploads/2019/02/ULI-Heitman-Climate-Risk-Report.pdf

[4] Asaf Bernstein, Matthew Gustafson, and Ryan Lewis, “Disaster on the Horizon: The Price Effect of Sea Level Rise,” Journal of Financial Economics (forthcoming), published online May 4, 2018; First Street Foundation, “As the Seas Have Been Rising, Tri-State Home Values Have Been Sinking,” August 23, 2018; Jesse H. Keenan, Thomas Hill, and Anurag Gumber, “Climate Gentrification: From Theory to Empiricism in Miami-Dade County, Florida,” Environmental Research Letters 13 (April 23, 2018); Jens Hirsch and Jonas Hahn, “How Flood Risk Impacts Residential Rents and Property Prices: An Empirical Analysis,” Journal of Property Investment & Finance 36, no. 1 (2018): 50–67; Athanasios Votsis and Adriaan Perrels, “Housing Prices and the Public Disclosure of Flood Risk: A Difference-in-Differences Analysis in Finland,” Journal of Real Estate Finance Economics 53, no. 4 (November 2016): 450–71.

[6] http://www.heitman.com/wp-content/uploads/2019/02/ULI-Heitman-Climate-Risk-Report.pdf

[7] https://www.fsb-tcfd.org/tcfd-supporters/