ESG reporting in line with updated HKEX guidance

In an effort to develop an increasingly informed market, the Stock Exchange of Hong Kong has updated its “How to prepare an ESG report?”, taking into account recent international climate-related disclosure recommendations and with an emphasis on the issuer’s governance structure for environment, social and governance (ESG) reporting. While CSR Asia welcomes the changes, issuers keen to align their reporting with updated guidelines are grappling with how best to revise their disclosures when interpreting the updated document.

With each iteration of the guidance document or reporting requirements, companies must recognise that far from being a box checking exercise, the production of an ESG report is a catalyst for vertical and horizontal communication within an organisation, assessment of risks and opportunities, and engagement of the members of the ecosystem within which the company operates.

Six steps of ESG reporting

To unlock the benefits of reporting, issuers should closely follow the updated recommended steps and procedures. In summary, the updated reporting guide advises issuers to:

- establish an ESG working group;

- understand the reporting requirements;

- determine the reporting boundary;

- conduct a stakeholder mapping and engagement exercise;

- determine the material ESG issues that are relevant to its business and prioritise the issues accordingly; and

- produce an ESG report covering: (a) a description of its ESG governance; (b) the reporting boundary; (c) a description on how it has applied the Reporting Principles under the Reporting Guide; (d) a report on each of the Reporting Guide’s “comply or explain” provisions; and (e) key messages that it aims to convey to investors and other stakeholders.

While the steps are clear, one key recommended disclosure enhancement in step 6 is causing consternation amongst reporting companies: reporting on compliance with relevant laws and regulations that have a significant impact on the issuer.

Reporting on compliance with relevant laws and regulations

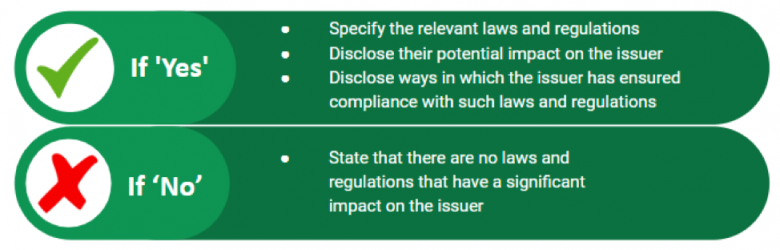

The revisions to the guide come as no surprise following HKEX’s analysis carried of ESG disclosure which found that some of the disclosures for Laws and Regulations were inadequate or not meeting the requirements. However, the use of the term ‘significant impact’ leaves room for interpretation and can present a challenge to the reporting company. The updated guide asks companies to consider whether there are laws and regulations in respect of an ESG Aspect which may have a significant impact on the issuer and proceed as follows:

Figure 1 Actions to take when determining whether business operations are significantly impacted by laws and regulations

As we see it, this inclusion in step 6 is closely linked to step 1, the establishment (or existence) of the ESG working group; step 3, determining the reporting boundary and step 5, determining material ESG issues. A logical process if answering ‘yes’ would be:

- The ESG working group determines the reporting boundary and material aspects.

- The group defines levels of significant impact on relevant aspects for each area of the business. The impacts could be categorised such as operational, financial, reputational.

- Departments or business units report to the working group with:

- the laws and regulations with which they must comply ranked for significance and including their main function(s)

- their impact on the business including the potential negative impact of non-compliance

- the management approach of the company in response to the regulation(s)

- This information is disclosed in the ESG report in a manner that satisfies the Board’s appetite for transparency and also aligns with the revised guidance document.

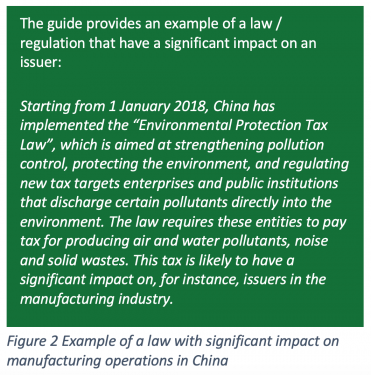

In relation to point 3, the step-by-step guide provides an example of a law that could have a significant impact on manufacturing operations in China (Figure 2). Other examples of laws and regulations with a significant impact to businesses could include the Banking Ordinance for financial institutions in Hong Kong or the EU Timber Regulation (EUTR) for companies importing timber into the EU.

In relation to point 3, the step-by-step guide provides an example of a law that could have a significant impact on manufacturing operations in China (Figure 2). Other examples of laws and regulations with a significant impact to businesses could include the Banking Ordinance for financial institutions in Hong Kong or the EU Timber Regulation (EUTR) for companies importing timber into the EU.

Whether issuers choose to include this information in the main body of the report, or conveniently annexed in a table is yet to be seen, and as with all reporting, the process will be refined with time. However, we are confident than when done effectively, the enhancement will enable senior management to better understand risks and mechanisms to mitigate against them.

The language of ESG reporting is too often littered with grandiose claims, throw-away statements and superficial nods to ‘complying with all laws and regulations’. What value do these add? With the updated guidance we can hopefully say goodbye to vacant claims of compliance and dive deeper into risk management and providing decision-useful information to investors. Companies should embrace this for the enhanced understanding it provides management and the richer ESG report it provides to stakeholders. For further information on how CSR Asia can help you prepare your next ESG report contact Aaron Sloan at aaron.sloan@elevatelimited.com.

Image source: https://www.cisco.com